Welcome to the latest edition of The Road to 2030 by Autotrader

The Road to 2030 Report tracks the progress of electric vehicle (EV) adoption in the UK using bespoke data and insights from Autotrader, the UK’s largest automotive marketplace.

The latest edition of the Report dives into market dynamics of the new and used electric sectors, exploring what’s working and where support is needed.

Published 11th June 2026

Opening remarks from Ian Plummer, Chief Customer Officer.

So far, 2026 has seen one key milestone after another in the electric transition: two million electric cars on UK roads, the average price of a new EV advertised on Autotrader falling below petrol for the first time and record high fuel cost savings to name just a few, we’ll highlight even more in this Road to 2030 Report. But while progress is positive and market dynamics appear to be moving in the right direction, there’s no guarantee these conditions are here to stay and we would caution against assuming they are.

Our previous Road to 2030 Report in February highlighted the disparities that still persist in the electric transition, from income to gender and geography. This Report will take a step back to look at a wider view of the market, exploring the impact of improved electric affordability and petrol price headlines, with a deep dive into the used electric market as we attempt to answer:

Is the electric market at a tipping point?

Context is key: geopolitics and consumer confidence

Rising fuel prices, driven by the recent Middle East conflict, are shaping consumer behaviour with clear jumps in electric interest that mirror the impact of Russia’s invasion of Ukraine in 2022.

With petrol prices repeatedly in the headlines, cost-conscious consumers have been checking out what electric cars fit their budgets, resulting in advert views of used electric cars on Autotrader overtaking available supply from the end of March.

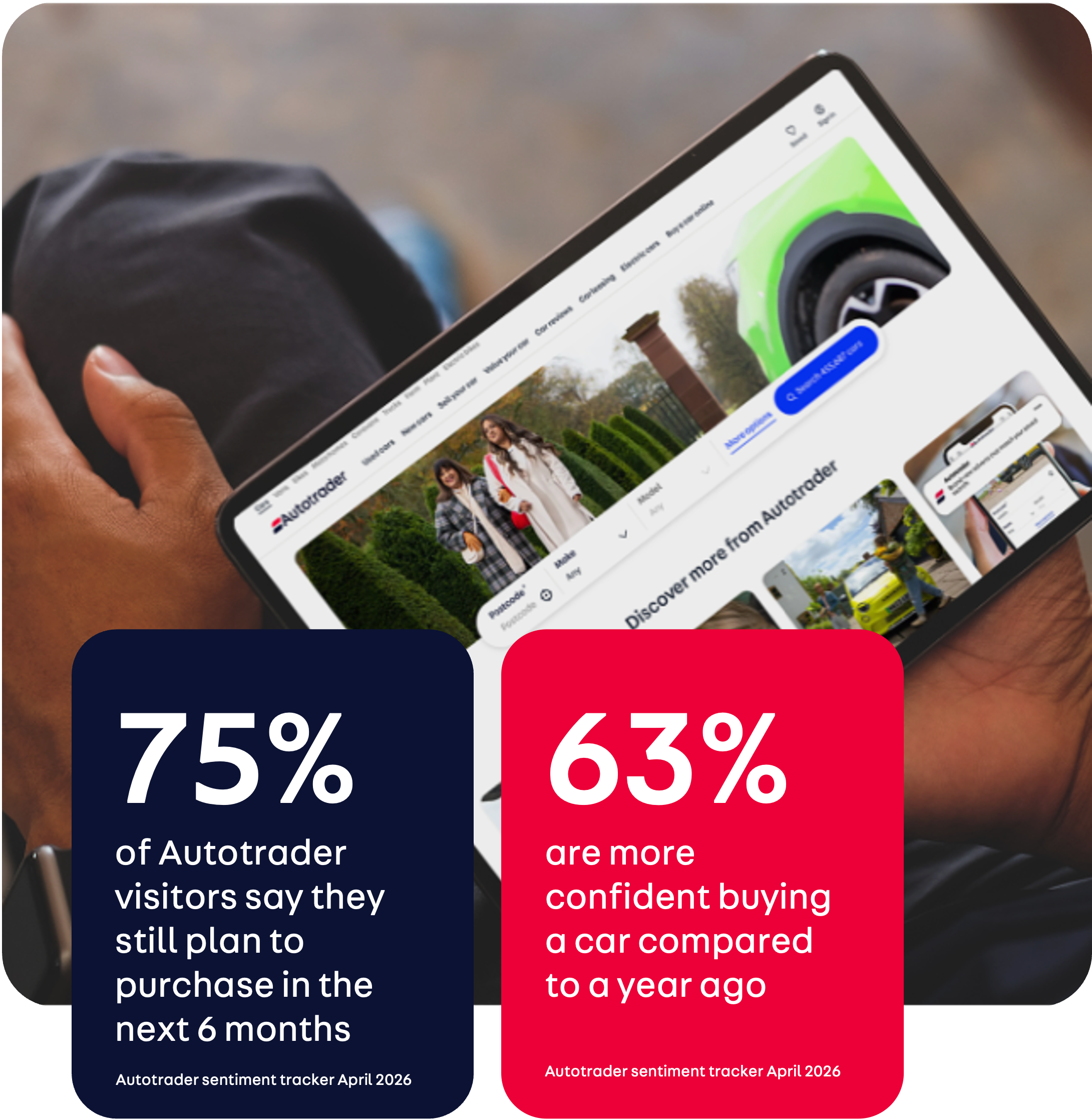

Despite broader pressures on consumer confidence, car buying activity remains resilient with 75% of Autotrader visitors saying they still plan to purchase in the next six months. Similarly, 63% of Autotrader visitors said they feel more confident in buying a car compared to a year ago, underlining the structural strength of demand in the automotive market.[1]

New EV market progress: steady, but not spectacular

Continued momentum in the new electric market is a positive sign. The growth in electric interest as well as adjustments and flexibilities recently introduced in the Zero Emission Vehicle (ZEV) Mandate mean that we expect to see compliance this year, as in previous years.

However, right now, we aren’t seeing the step-change that is required to hit the steep annual targets that are coming in the next few years of the Zero Emission Vehicle (ZEV) Mandate.

Where are we now?

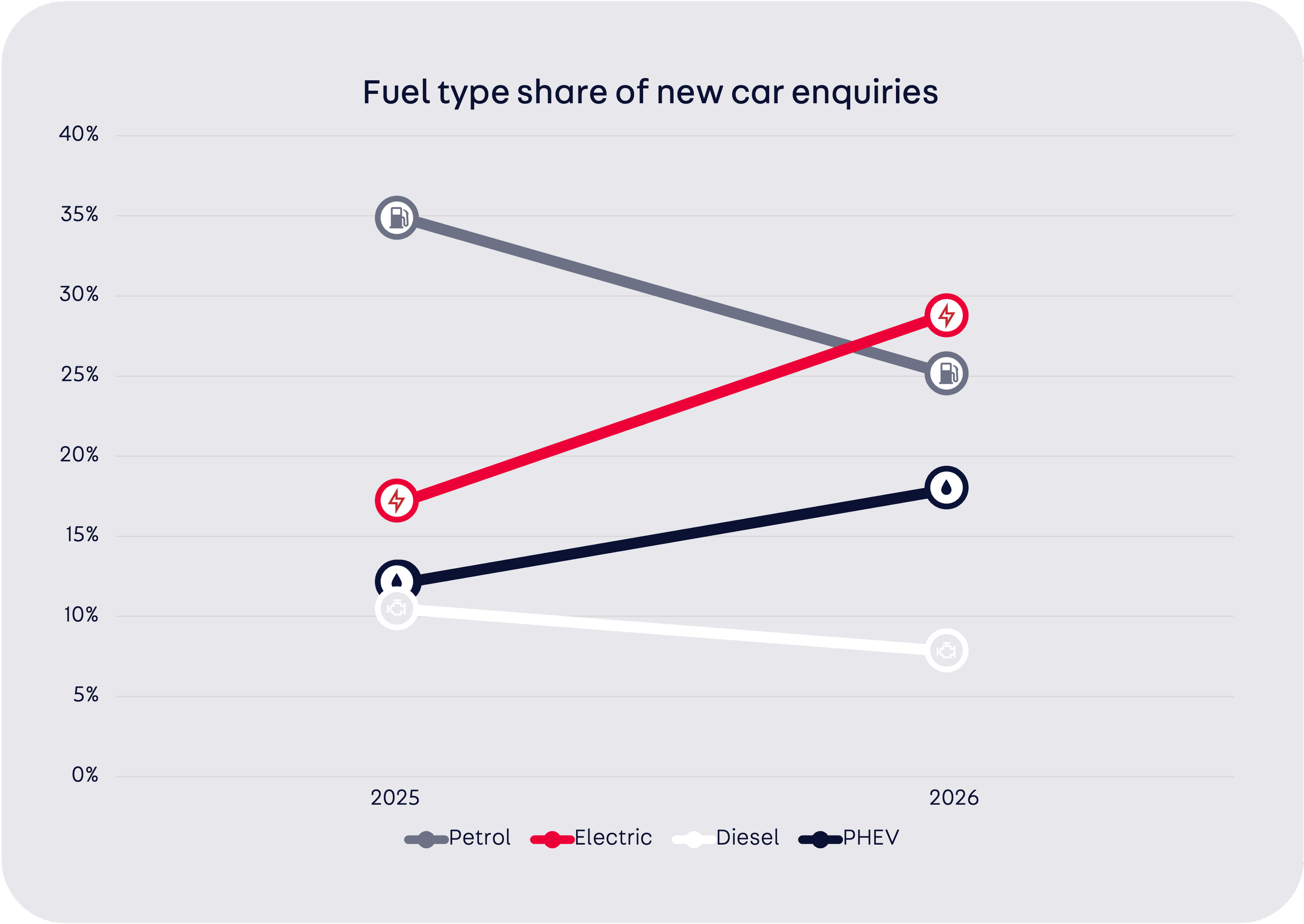

EVs currently account for more than 27% of new car sales year-to-date, up from 21.8% this time last year.

Milestone

In April, EVs were the most popular new car fuel type on Autotrader for the first time ever, taking 29% of new car enquiries. This continued into May.

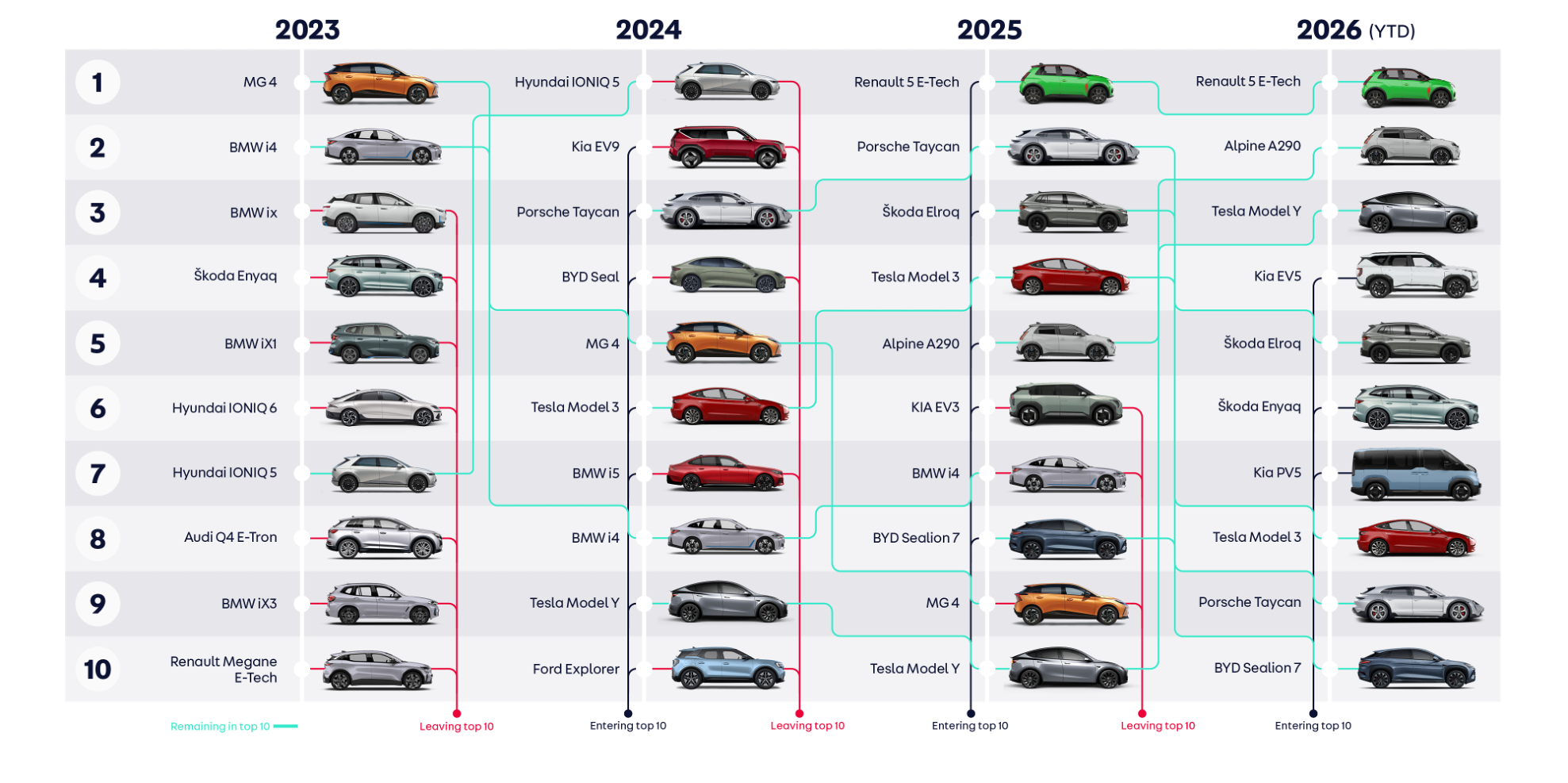

The continued growth in affordable models is vital

to achieving rapid acceleration of electric adoption in new car sales. The top electric model list is frequently dominated by smaller, more affordable cars, thanks also to the support from the Government’s Electric Car Grant.

Most popular EV models based on ad views

Milestone

In March, the average advertised price of new EVs fell below petrol for the first time ever.

Is this a breakthrough moment for affordability?

This continued in April but reversed in May as new EVs ended up on average £13 more expensive than new petrol cars on Autotrader. This includes all discounts from manufacturers, retailers and the Government’s Electric Car Grant.

How did we get there?

The closing of the pricing gap – that £13 difference in May was £3,607 in 2025 - has been driven by increased manufacturer discounting as the industry strives to comply with the ZEV Mandate.

The number of smaller and more affordable models is growing thanks to the millions invested by the industry in research and development resulting in lower battery and production costs, and this is resulting in increasing consumer interest.

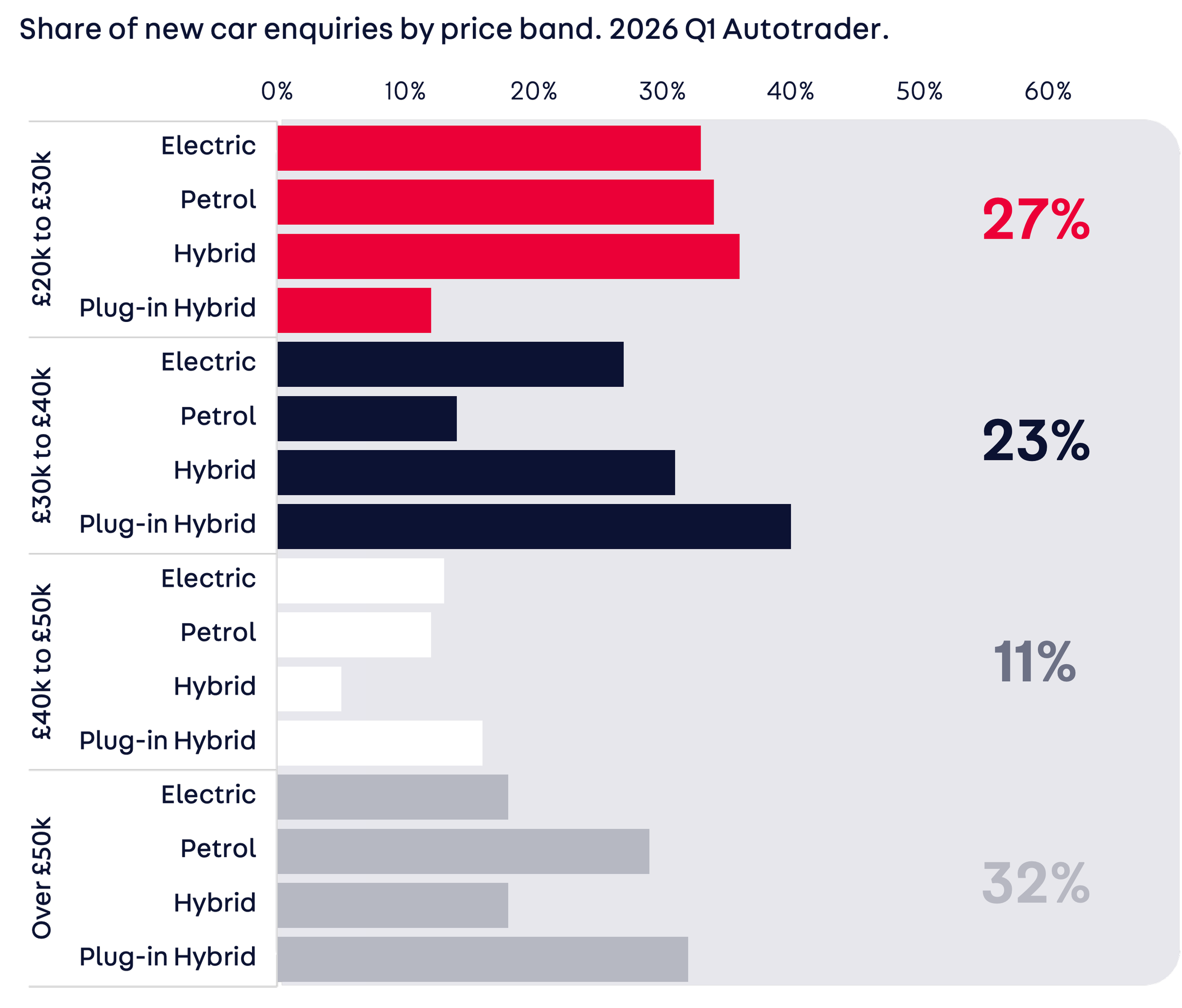

Data shows the majority of electric enquiries are now in the £20,000-30,000 price bracket. The good news is the number of models below £30,000 continues to grow:

What about the used market?

Used prices are now stable following 30 months of year-on-year (YoY) price drops that remain a big concern for industry.

Milestone

In May, used EV prices were flat YoY, marking the first time EV pricing has been non-negative since December 22.

This price growth is predominantly coming from the 3-5 year old age group and we’ll monitor to see the impact of this on consumer demand.

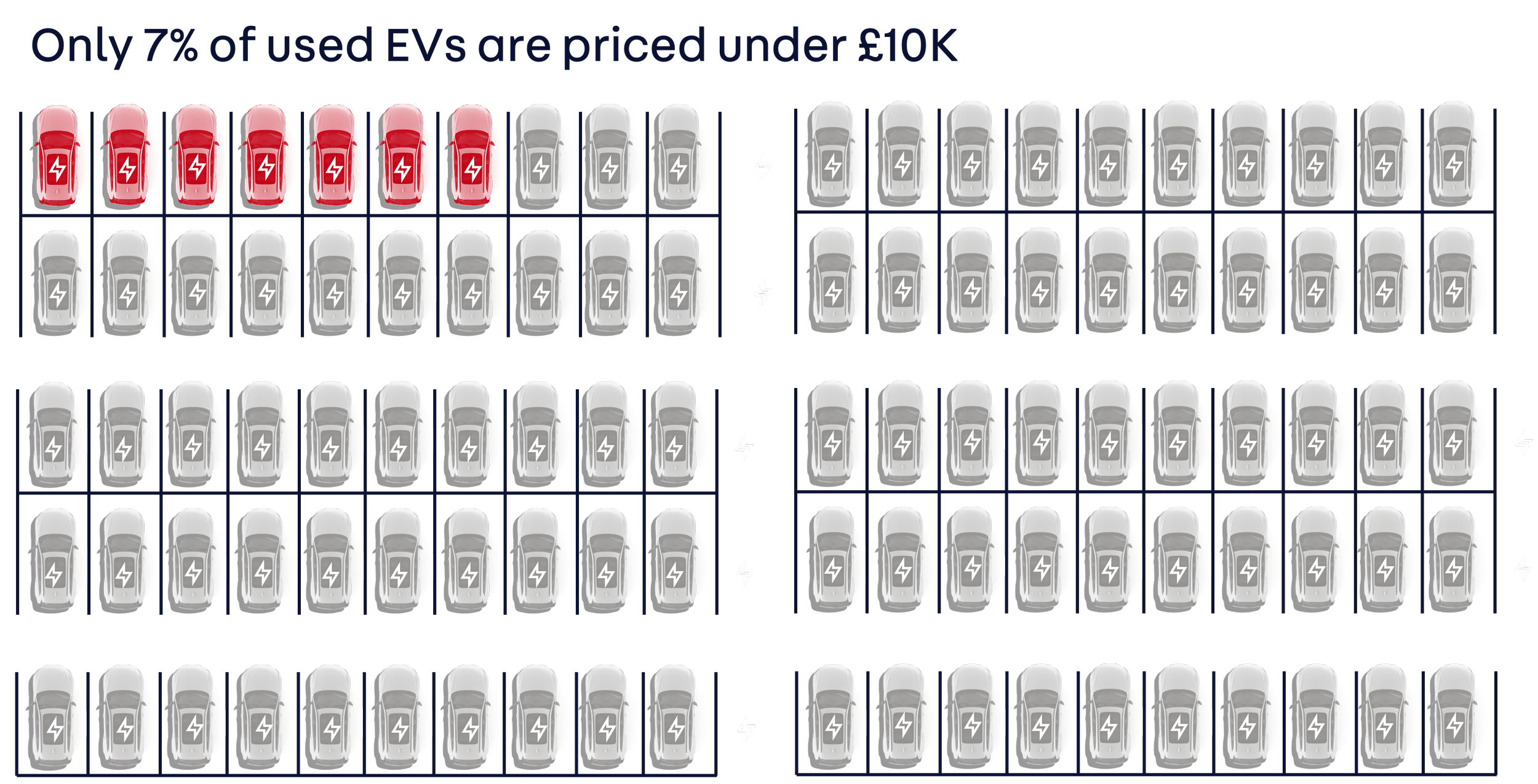

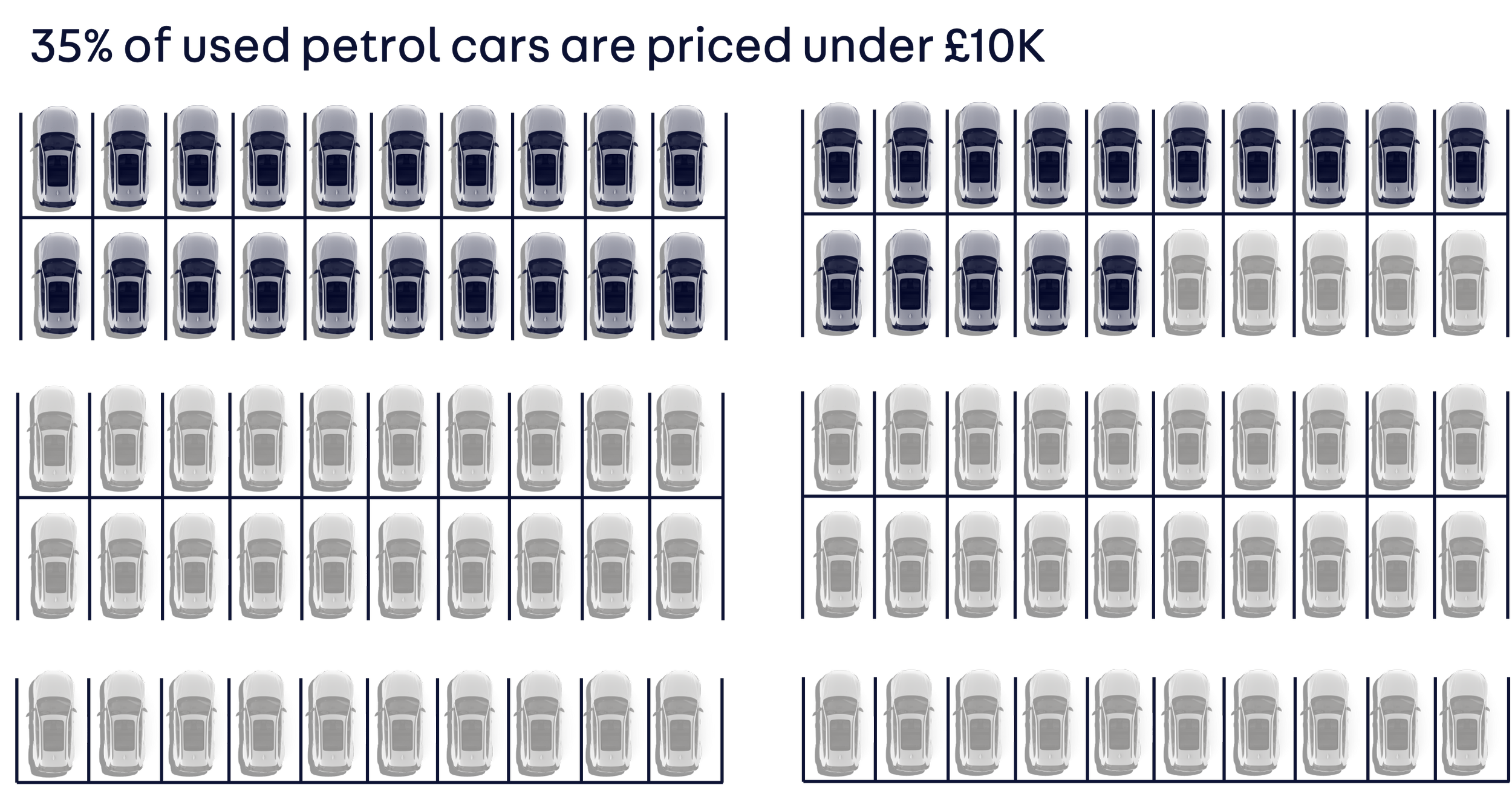

At the affordable end of the used market, under £10,000, we’re still seeing a lack of supply - meaning that lower income households are still being locked out of the electric transition.

Spring 2026: the EV tipping point?

Demand is rising across all EV age cohorts, with strongest growth in 3–5-year-old vehicles where interest has doubled year-on-year. These trends indicate that we’re seeing progress towards maturity as the used electric market begins to more closely resemble the wider used car market.

Milestone

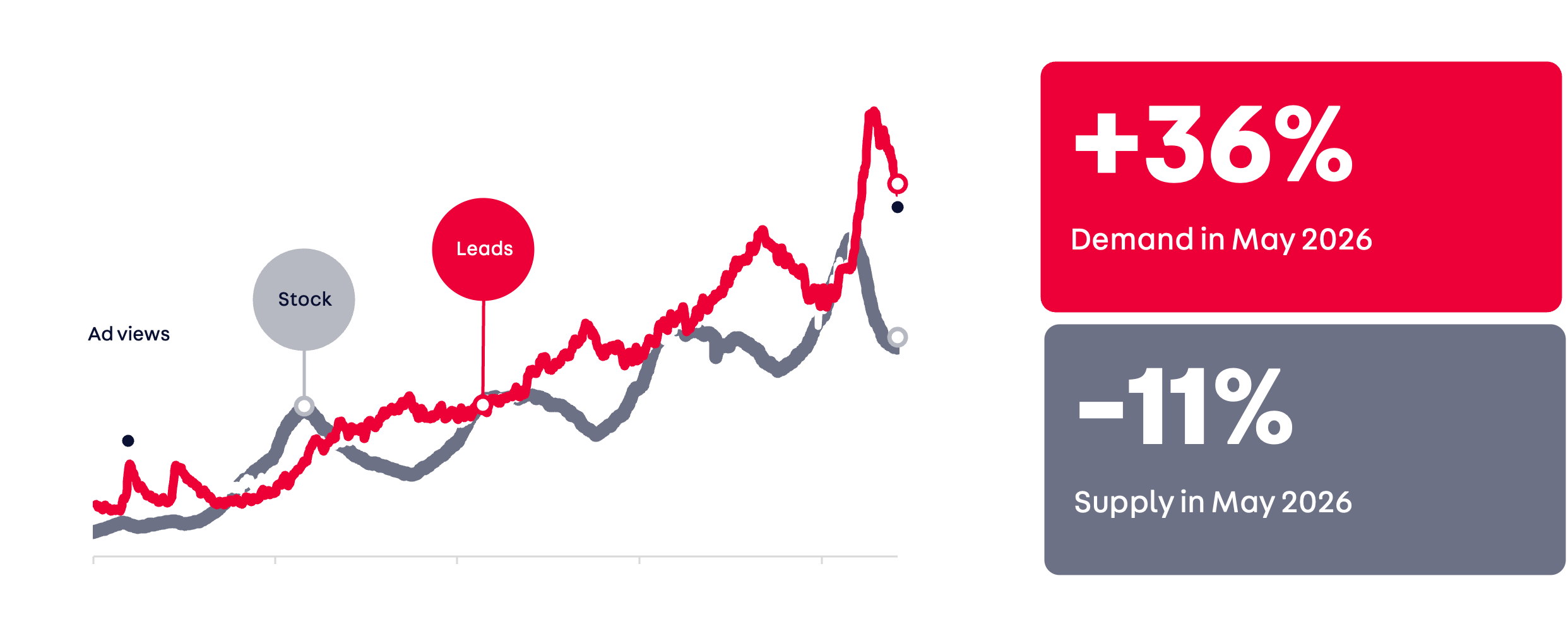

In April, supply of used electric cars on Autotrader fell for the first time ever as interest converted into sales, resulting in stock being removed from the platform.

This resulted in demand for used electric cars outstripping supply for the first time ever on Autotrader.

However, depreciation is still steep in the 0–3-year age bracket, evening out as cars pass the 3-year mark, at which point used EV pricing matches petrol equivalents. This means there’s exceptional consumer value in the 3+ market, especially as fuel prices remain elevated, meaning EVs can unlock record high fuel cost savings.

Right now, the speed of the growth is encouraging and current levels of retailer engagement is positive, we’ll monitor to see how this changes over time.

How are retailers responding?

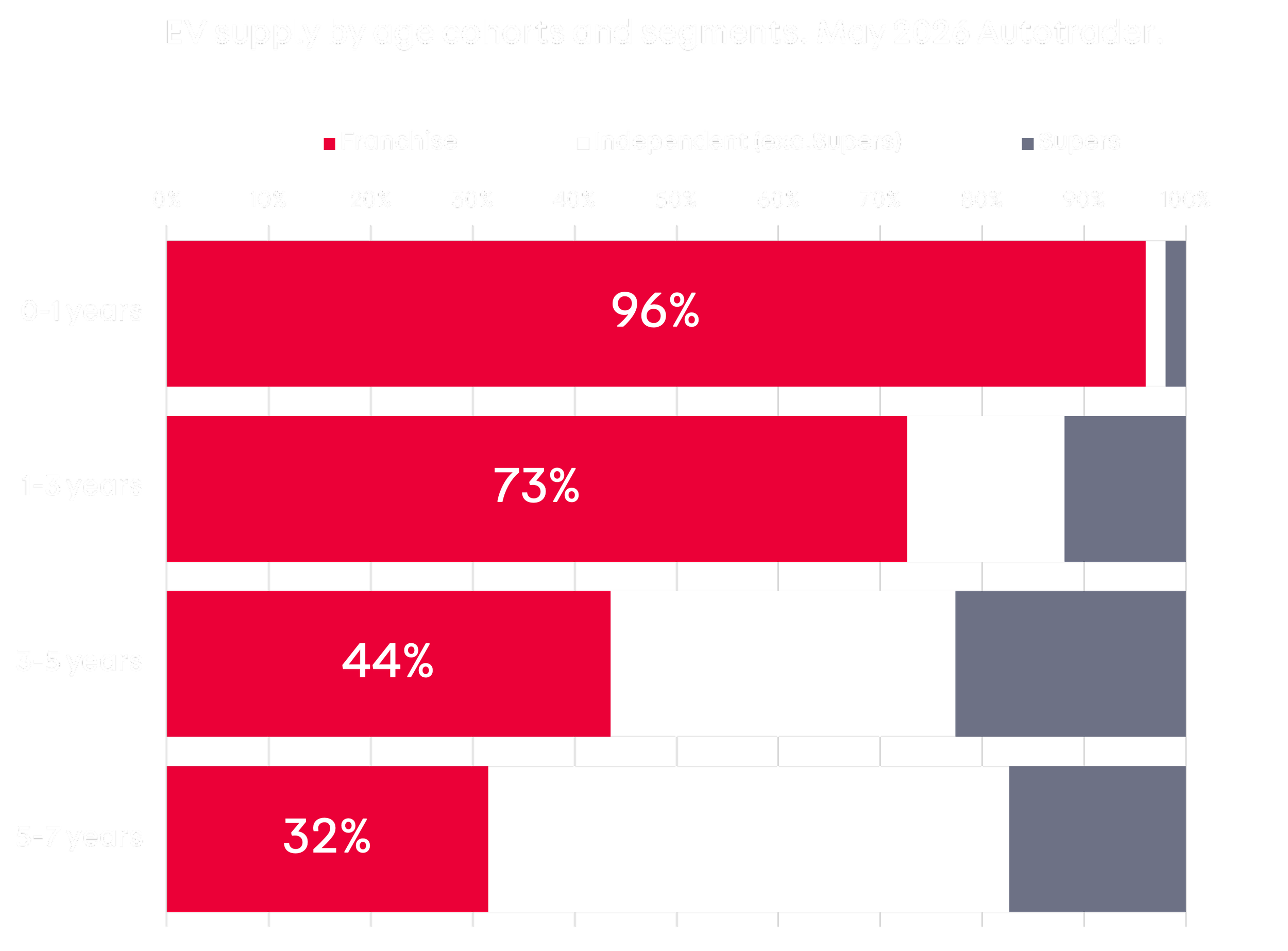

The data shows that a third of retailers who sell cars aged five years and under have stocked an electric car, this drops to a fifth for retailers stocking 5-7 year olds cars. It’s important to remember not every retailer needs to sell EVs, those focusing on the 10+ segment of the market have a few years before any significant volume flows through to their forecourt.

Right now, the speed of the growth is encouraging and current levels of retailer engagement is positive, we’ll monitor to see how this changes over time.

Is this level of growth likely to continue – is this the much-anticipated tipping point?

Whilst we’re making good progress, it doesn’t seem likely that this is any kind of substantial tipping point.

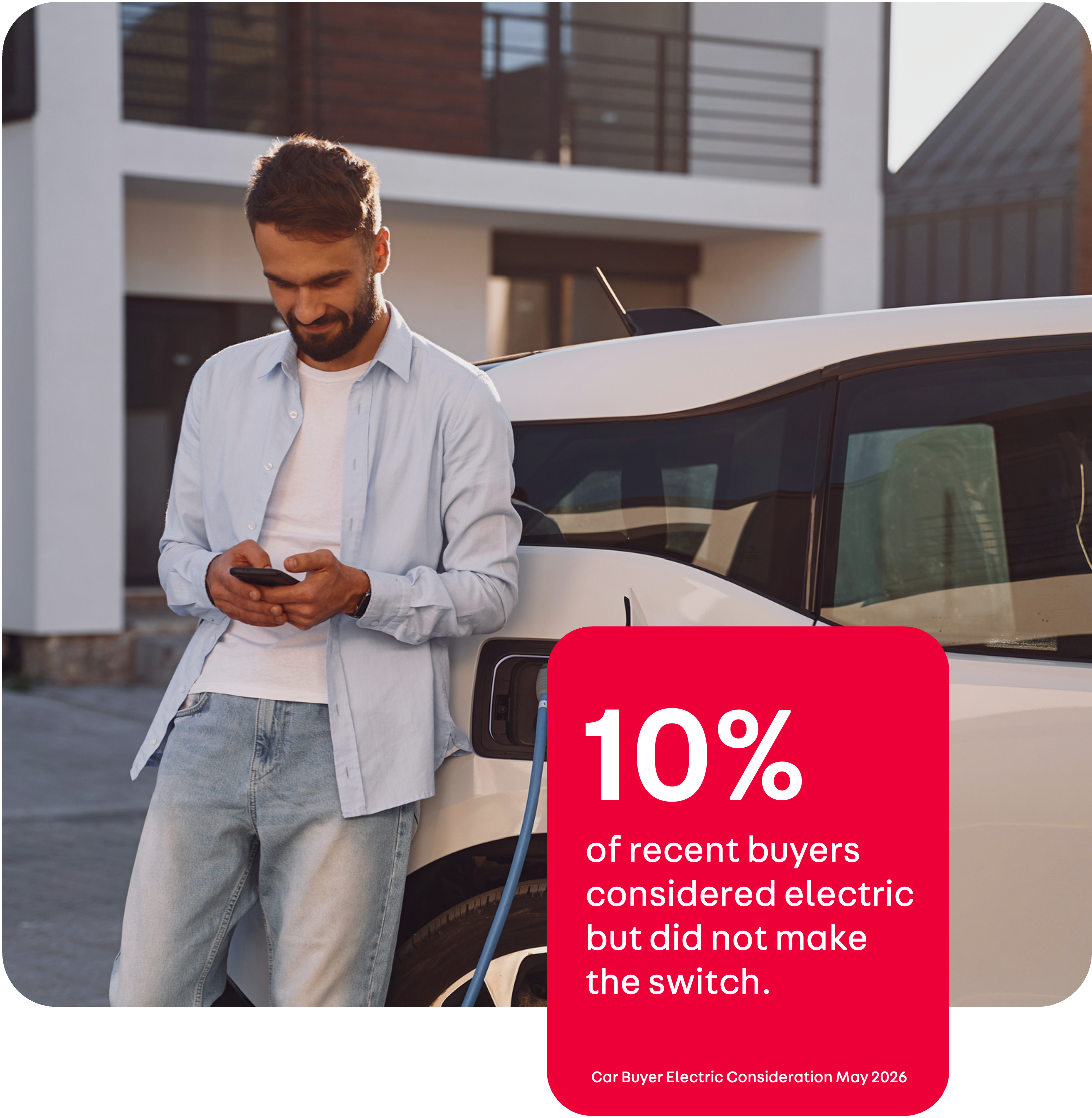

We commissioned research to explore the attitudes of consumers who bought a new or used non-electric car in the last six months. We were especially interested in those who bought in the last three months, since petrol prices spiked, following the conflict in the Middle East.

Results show that just 10% of recent non-electric car buyers[2] even considered going electric, suggesting there’s work to do to increase consideration levels.

The age group with the highest level of electric consideration were 30-34 at 14%. Just 8% of petrol buyers and 7% of diesel buyers considered electric.

What stopped them?

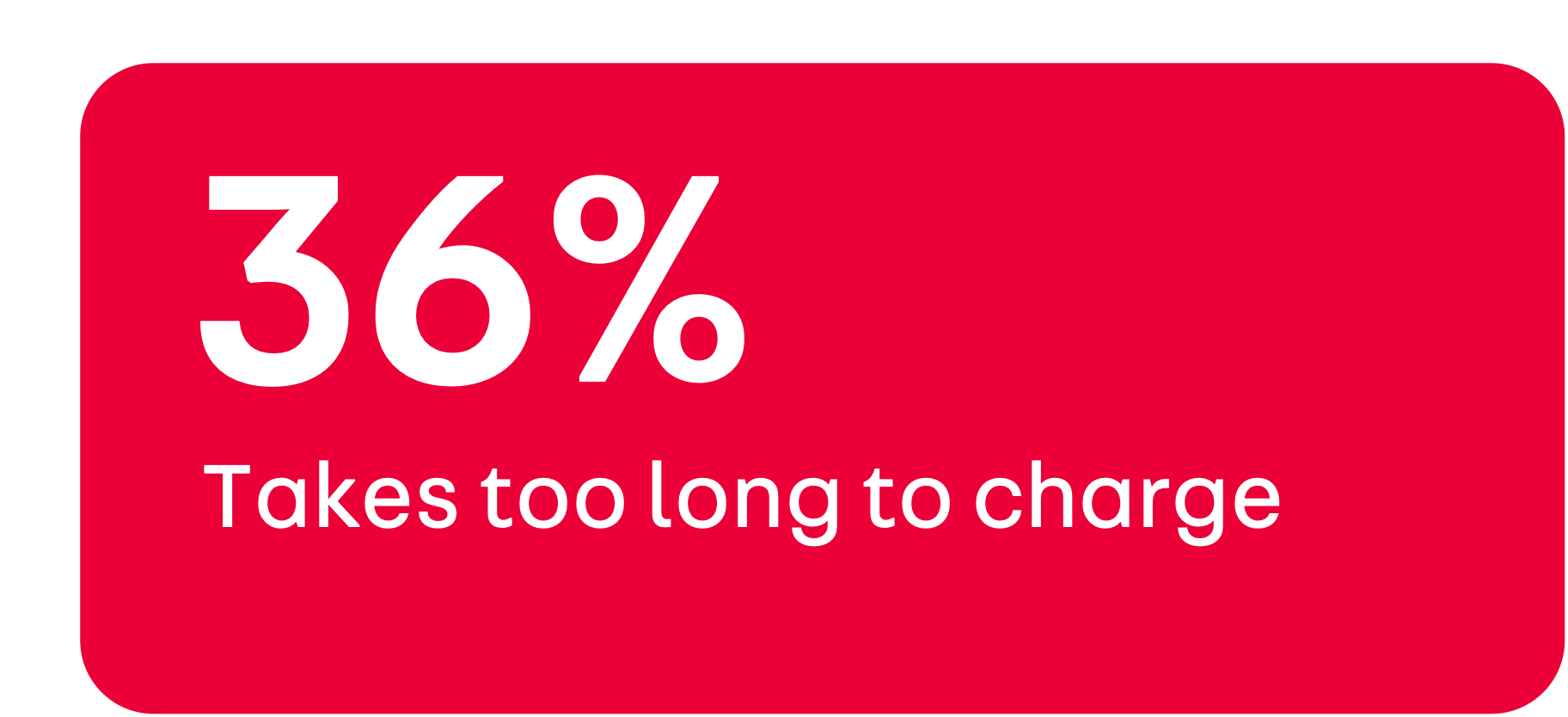

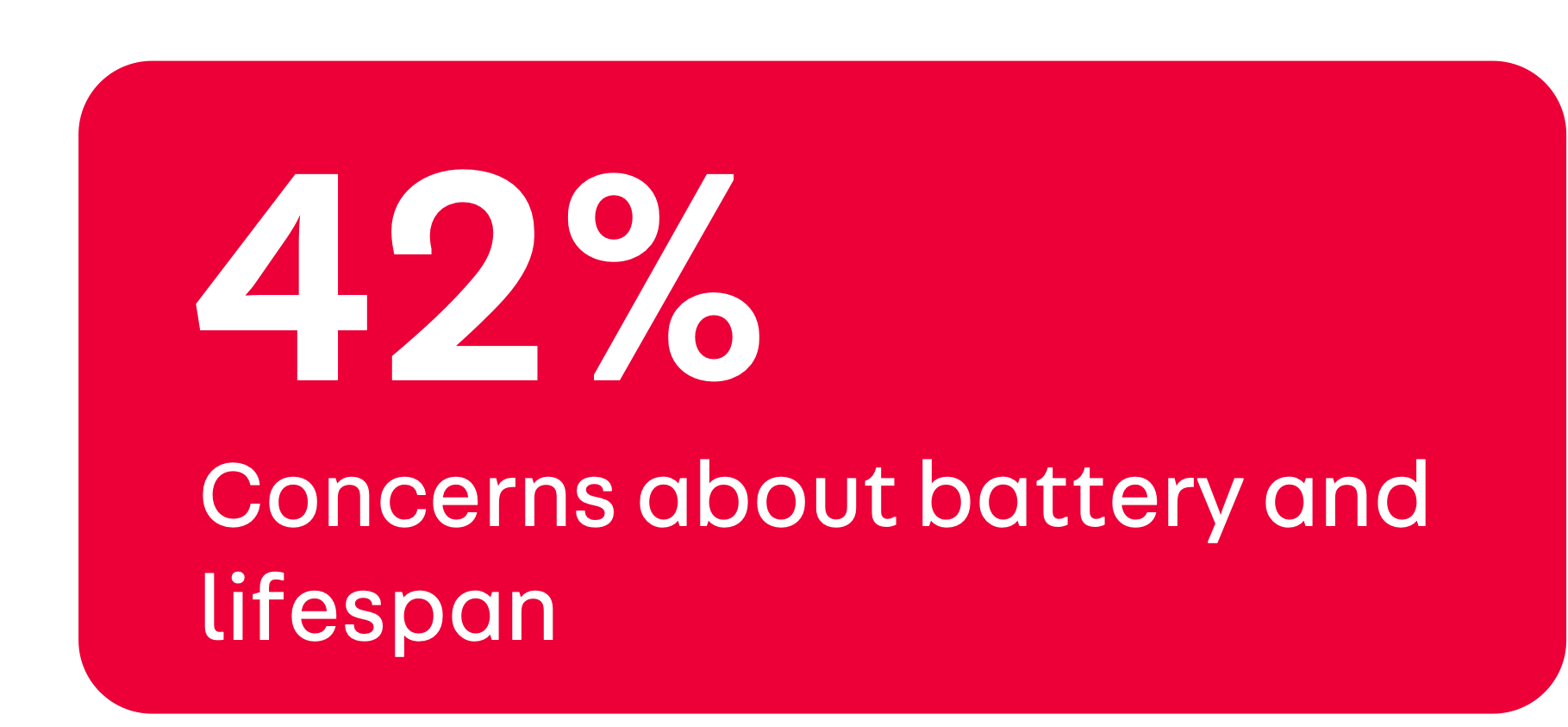

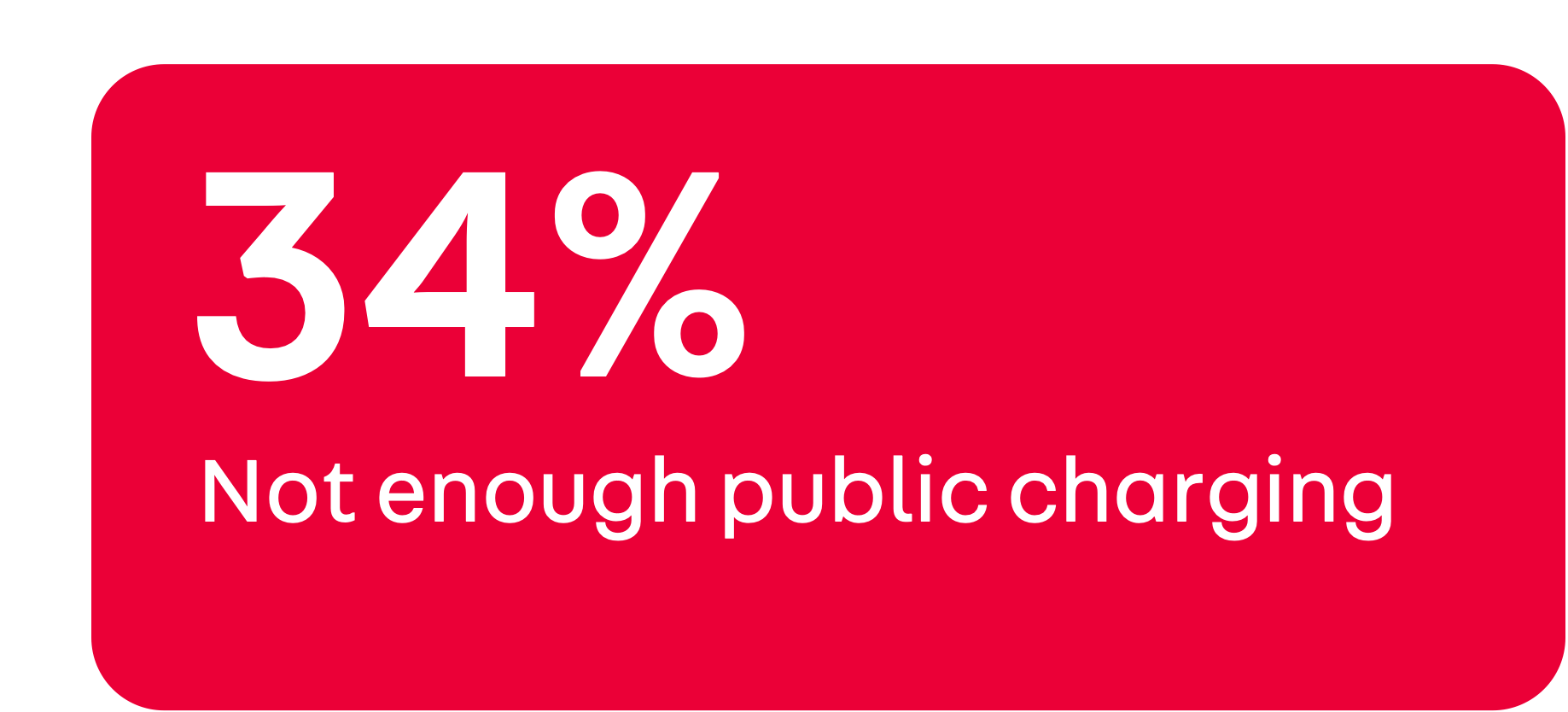

53% of the considerers told us they thought electric cars are too expensive. The next biggest barrier was not being able to drive far enough on a single charge with 28% citing this as a barrier, followed by concerns around availability and price of public charging at 23% and 22% respectively.

Why didn’t others consider?

The top barrier to making the switch is still price, with half of all non-considerers stating this. Here’s a full list of barriers:

34% of respondents also told us that electric cars don’t align with their personal values.

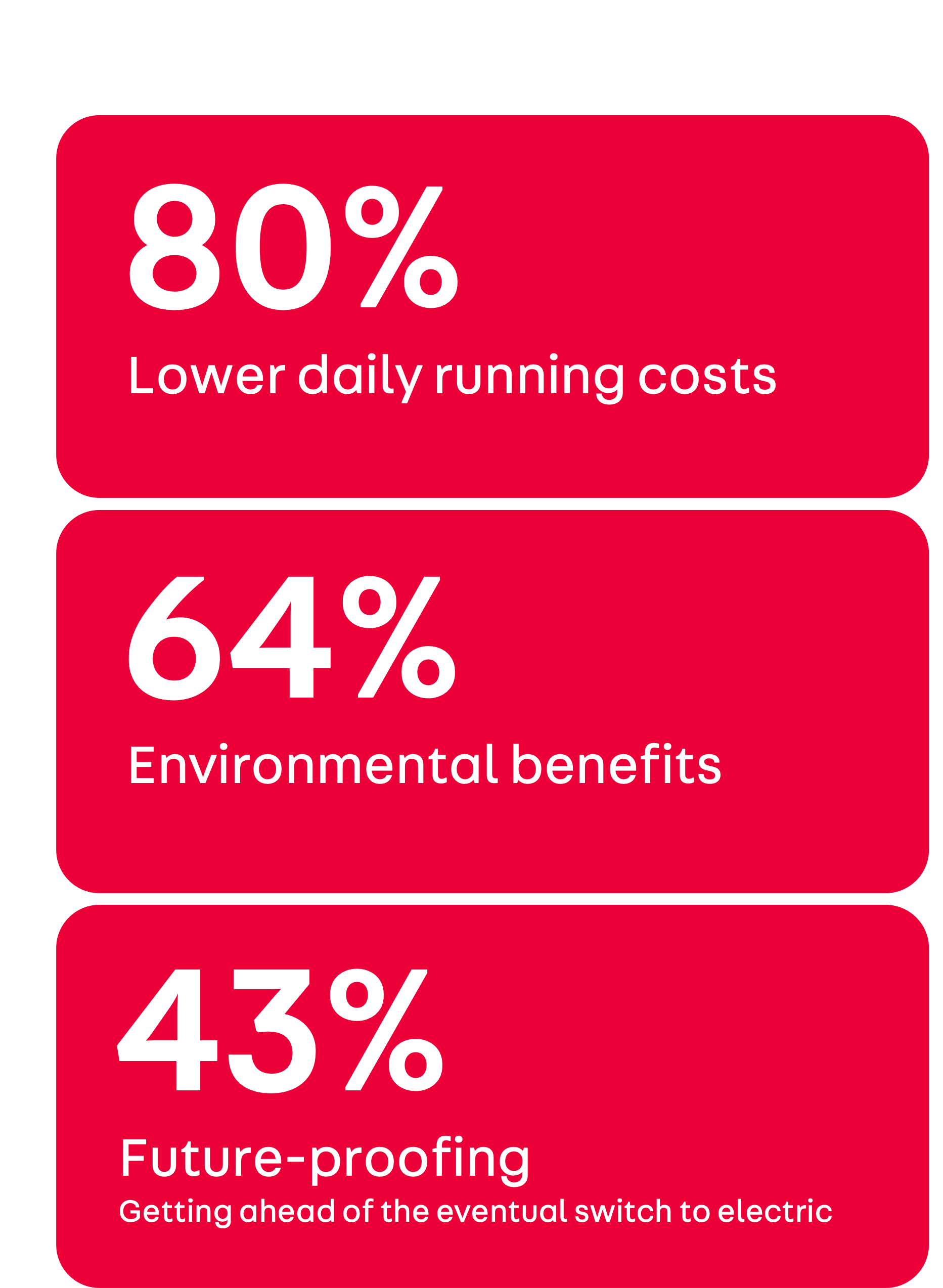

More than eight in ten buyers (84%) think electric cars are expensive to buy, seven in ten (69%) find charging inconvenient, and almost two-thirds (65%) say there are not enough places to charge near their homes.

How do concerns differ between considerers and non-considerers?

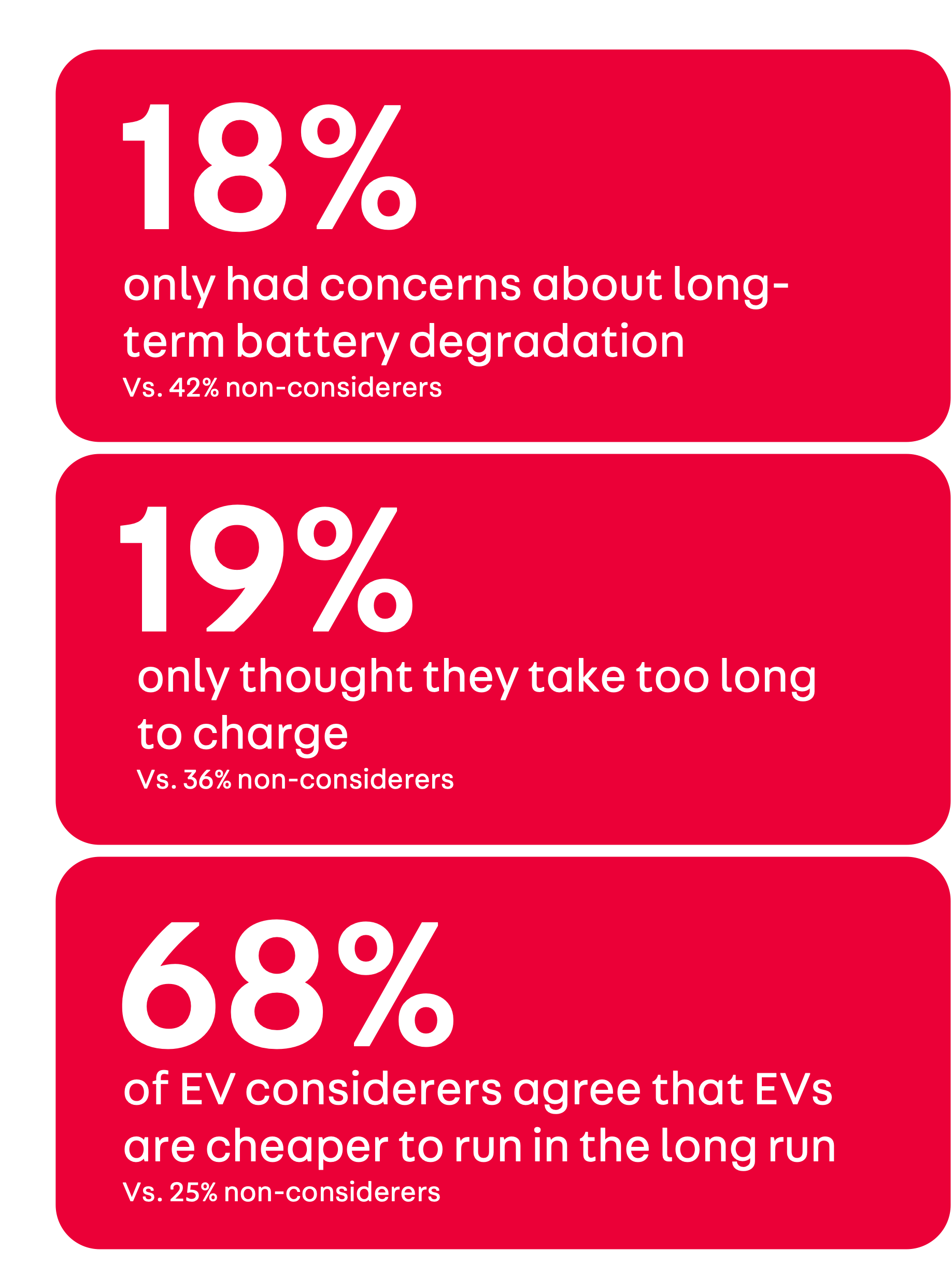

Whilst there was consistency with price being the number one blocker for both groups, with around half saying this was a concern, there were many areas where considerers were far more positive about EVs than non-considerers. Considerers were much more informed:

A little bit of knowledge can go a long way

This suggests those who are more informed about electric vehicles and have done their research on battery health and charging times, are more likely to consider. This then strengthens the argument in our January 2026 No Driver Left Behind Report: Bridging the EV income gap, that there are large groups of informed drivers who are ready to make the switch but simply can’t afford to.

Unfortunately, this data also shows we still have a big issue with getting the right information to the right people and encouraging independent research about how an electric car might benefit individual drivers. The new research also reconfirmed past findings that certain groups of society are at higher risk of being left behind in this transition. For example, women were more than twice as likely to state that lack of knowledge about EVs is stopping them from buying one (8% of men said this vs 17% of women). Similarly, confidence in EV knowledge levels jumped after household income crossed the £80,000 mark.

But things look positive right now - won’t this continue?

There’s a risk here that rather than recent events converting a brand new cohort of electric considerers into purchasers, we’ve just pulled forward those who would have converted next anyway. Electric enquiries doubled on Autotrader since the end of February when the conflict broke out in the Middle East but there’s no guarantee this will continue.

Current market conditions could also echo the sales bump we saw in March 2025, ahead of new tax changes that increased the cost of driving an EV. The March boost was followed by a smaller April, as those who were considering buying electric bought their purchase forward. This could also mimic 2022 when, following Russia’s invasion of Ukraine, the electric market experienced a boost as petrol prices soared, but this didn’t resolve the barriers and nor did it set the transition on an inevitable path to success.

EVs still make up just a small proportion of all car sales, their prices are still out of reach for many buyers and structural inequalities around access to charging remain. Whilst this isn’t any kind of definitive tipping point, it’s certainly a timely boost.

So what does the Government need to do?

In summary,

The transition to electric vehicles is making good progress, in large part due to significant investment from the industry, with the used market playing a critical role in driving mass adoption. However, currently, this isn't an organic transition - it's reliant on outside factors such as conflict and cost of living issues. With social proof being a key driver of electric consideration, we can hope that the current boost in electric sales will have a ripple effect in awareness and positivity towards EVs.

However, affordability at the lower end of the market remains the key barrier and will be for some time. For example, in 2035, just 15% of 10–15-year-old stock will be electric. What does 15% of a market look like? For context, right now 15% of 10 year old cars are blue, 11% are Fords and 7% are Saloons.

Spring 2026 may prove to be an important catalyst, but it is too early to determine whether a true tipping point has been reached. Right now, it feels like we are teetering and it’s unclear if progress will continue. A steadier, healthier transition would not be reliant on global conflict and domestic cost of living pressures but driven by the positive pull of a range of attractive electric cars available at an affordable price for every driver, confidence in public charging infrastructure and fair access to cheap charging for everyone.

References

[1] Autotrader sentiment tracker April 2026

[2] Bought a car that was not fully electric in the last 3 months, 1200 respondents. 10% consideration for full sample of 2,000 respondents. May 2026.

[3] EV knowledge concerns of households income (HHI) £20,000-£79,999 was on average 14% vs 5% of people with HHI above £80,000.